Navigating the real estate market in the Beehive State can be daunting, but understanding how to get a mortgage is the first real step toward homeownership. Many prospective home buyers start their journey by exploring the financial landscape of home loans —the real competitive edge comes from securing a mortgage pre-approval. This document proves to sellers that a mortgage lender has already vetted your finances and is ready to back your offer.

To start the process, you should research the best mortgage companies and best mortgage lenders available in the state of Utah. Experts encourage you to get a mortgage quote from several different sources to ensure you get the best deal. While some buyers prefer large national banks, others have found that working with a local mortgage broker offers help with the local markets and a more personalized experience.

What You Need to Get Pre-Approved

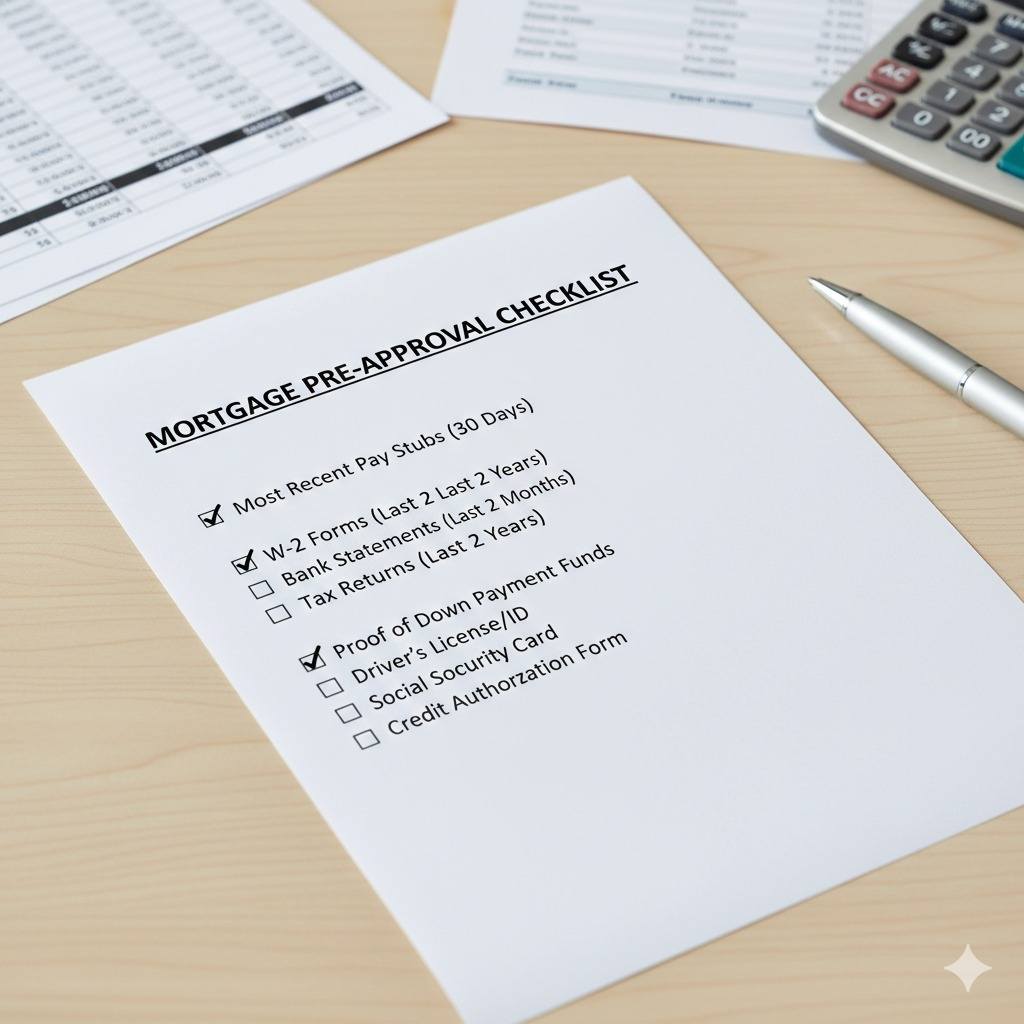

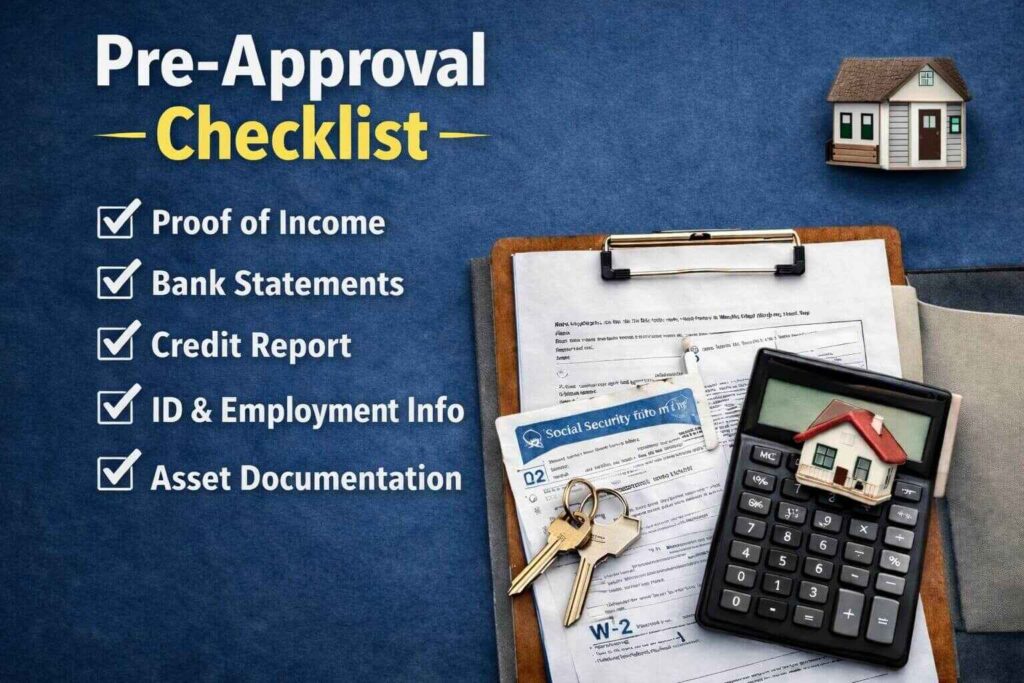

When you sit down with a professional to discuss your mortgage application, you might ask, “What will I need to get a mortgage?” Generally, you will need to provide proof of income (such as W-2s and tax returns) and evidence of assets for a down payment. Knowing specifically what you need for pre-approval saves time and stops the underwriting process from stalling.

Once you have gathered your documents, the next question is timing. When should I apply for the mortgage loan paperwork? Ideally, this should happen before you even set foot in an open house. When should a lender pre-approve my mortgage loan? Most experts recommend getting your letter 3 to 6 months before you intend to buy. This gives you time to fix any credit issues that might arise during the steps to buying a house. When should you get a mortgage pre-approval? As soon as you are serious about entering the market.

Understanding Home Loan Interest Rates and Programs

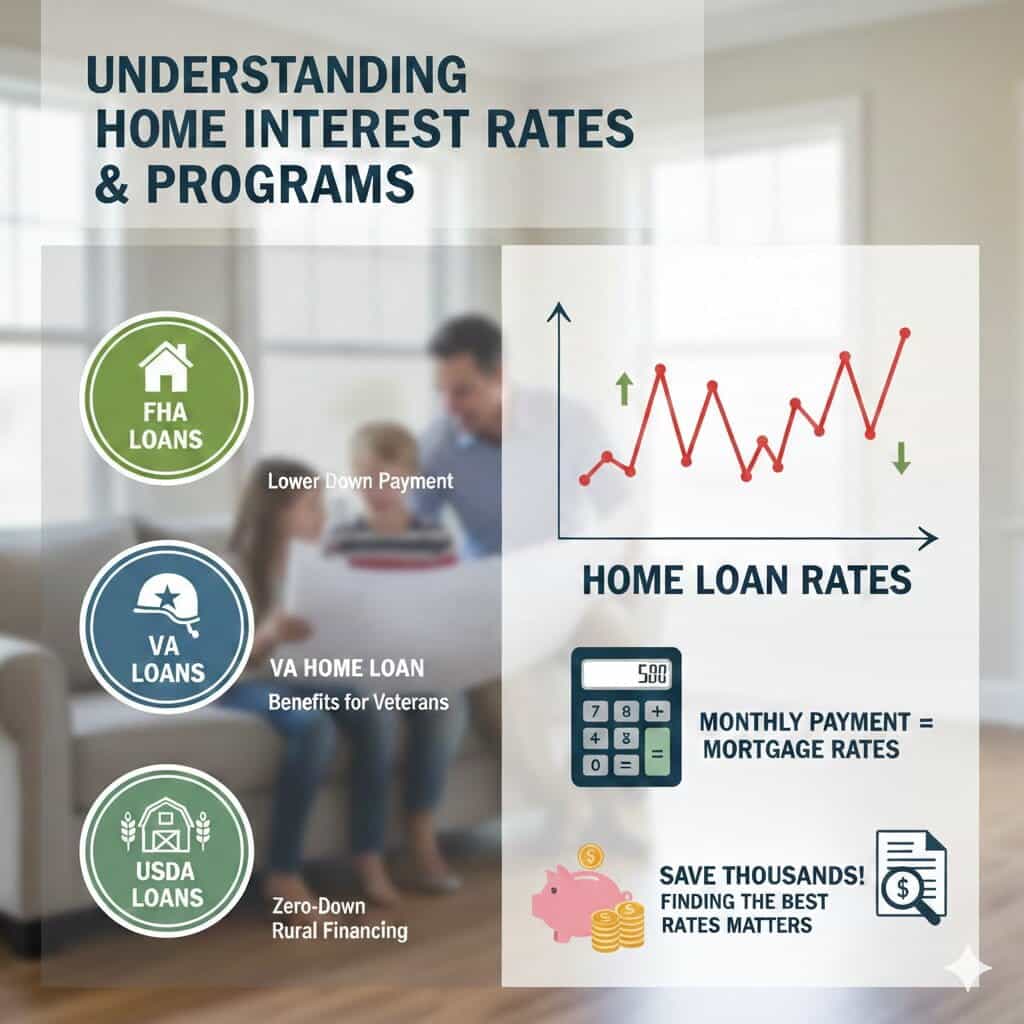

Your choice depends on your financial situation and specific program requirements. For many, FHA loans are an excellent entry point because they offer lower down payment options. Veterans should always look into a VA home loan, which provides significant benefits for those who have served. In more rural Utah communities, USDA loans are another powerful tool for zero-down financing.

Regardless of the program, current mortgage rates and home loan interest rates dictate your monthly payment. It pays to be diligent; finding the best mortgage or home loan rates can save you thousands of dollars over the lifetime of your loan. Keep a close eye on home loan rates, as they fluctuate with market conditions.

Finalizing Your Mortgage Pre-Approval in Utah

It is important to understand the difference between securing a home loan approval and obtaining a prequalification for a home. A pre-qualification is a surface-level look at your debt, while a pre-approval is a deep dive into your credit score. Most sellers in Utah will not even look at an offer without a formal pre-approval letter. As you finalize your plans, continue to monitor current mortgage rates and stay in close contact with your lender. Following these steps will position you to secure your dream home. Whether comparing lenders or quotes, preparation is the key to success.

The Utah housing market is shifting, and in 2026, the traditional path to homeownership is being rewritten. For many residents, securing a Mortgage no longer means walking into a bank with a simple W-2. As the “Silicon Slopes” continue to foster a culture of independence, more buyers are entering the market as self-employed professionals, a 1099 contractors, or a Gig-worker.

While these roles offer freedom, they often complicate the Pre-approval process. Understanding the specific Eligibility requirements for non-traditional Income is the first step toward moving from a rental to a home you own.

Utah Mortgage Strategies for the Self-Employed and 1099 Earners

For a Self-employed individual, the biggest hurdle is often proving a stable Income when tax write-offs reduce your “on-paper” earnings. In 2026, lenders have become more flexible, offering Bank Statement loans that look at actual deposits rather than net tax figures. This is a game-changer for the Gig-worker who may have multiple revenue streams.

When applying, having a CPA-prepared P&L (Profit and Loss statement) can significantly boost your Credit profile’s credibility. Whether you are looking for a Conventional loan or a government-backed FHA product, documenting your financial health accurately ensures you don’t hit unexpected Limits during underwriting.

First-Time Buyer Grants and Downpayment Assistance

If you are a First-time buyer in Utah, you have access to some of the most aggressive financial Assistance in the nation. The state continues to offer significant Grants and Subsidies designed to bridge the gap between savings and rising home prices.

Currently, a popular Utah program provides up to $20,000 for a Downpayment, which can be applied to newly built Construction. For those with a military background, VA loans remain the gold standard, often requiring $0 down. Similarly, buyers looking at rural or suburban growth boundaries may find that USDA loans offer zero-down Eligibility for those who meet specific household Income benchmarks.

Investor Opportunities and DSCR Loan Limits

The 2026 market isn’t just for primary residents; it’s a prime environment for the savvy Investor. If you are looking to acquire a rental property but want to avoid the strict debt-to-income ratios of a Conforming loan, a DSCR (Debt Service Coverage Ratio) loan is the ideal tool.

DSCR loans qualify the property based on its own potential rental Income rather than your personal salary. This allows investors to bypass traditional Mortgage hurdles, making it easier to build a portfolio of Utah real estate. Even if you are a Veteran investor or a professional with a complex 1099 tax history, these asset-based loans provide a streamlined path to closing.

Refinance and Market Outlook

As we move through the year, many homeowners are keeping a close eye on the market to refinance existing high-interest debt. Whether you are looking to lower your monthly payment on a Conventional loan or tap into equity for home improvements, understanding the current Utah rate environment is essential. From the specialized needs of the Self-employed to the broad Assistance available for a First-time buyer, the 2026 housing landscape is built on flexibility. By mastering your Credit and choosing the right loan product—be it FHA, VA, or DSCR—homeownership in the Beehive State is more attainable than ever.

The real estate landscape in 2024 is moving at a rapid pace. For many Utah residents, the primary barrier to entry is understanding the financial path to homeownership. Data from the April 2024 to March 2025 period shows a 900% surge in interest for foundational financing terms. This signals a highly active and competitive market. Looking at current conditions, many prospective buyers are starting their journey with the same fundamental question: ‘Can I get approved for a home loan?’ This guide is designed to clarify the procedural gaps in the market. It provides you with a definitive roadmap from the first inquiry to the final closing.

For many, the process begins when they start browsing listings. They often wonder when to get prequalified for home loans. In a market as competitive as Utah’s, the answer is almost always to start as early as possible. This initial stage often involves a quick mortgage prequalification. It gives a high-level overview of your purchasing power based on unverified information you provide to a lender. Since this step usually doesn’t involve a deep credit pull or extensive background checks, you can often receive a mortgage prequalification estimate almost instantly. This gives you a vital baseline for your search.

If you are unsure of the mechanics, learning how to get prequalified for a home loan is simpler than most expect, though it requires honesty about your financial health. You will generally provide basic details regarding your gross monthly income, existing debts, and potential down payment savings to a mortgage professional. Getting prequalified for a mortgage early helps you focus on properties within your price range by providing a clear prequalification estimate. While this is a non-binding step, it serves as the essential “starting line” for any serious buyer navigating the 2024 market.

Navigating Home Loan Pre Approval and Utah Affordability

Once you transition from casual browsing to serious offer-making, you must get approved for a mortgage in a more formal and documented capacity. A loan preapproval mortgage is much more robust than a simple prequalification. It involves a lender verifying your tax returns, W-2s, and bank statements to provide a documented commitment for a specific loan amount. In 2024, the digital shift has made obtaining a home loan preapproval online easier than ever. This method has seen a 900% increase in search volume, as buyers prioritize speed and accessibility.

The most frequent query I see for active hunters in Utah is where can I get pre-approved for a home loan. Working with local experts who understand regional property taxes and Utah-specific insurance requirements can be a major advantage when competing against out-of-state offers. To begin this formal stage, you will follow the necessary steps to get approved for a mortgage. This includes a formal credit pull and a comprehensive debt-to-income analysis. Once completed, your lender will issue a mortgage preapproval estimate. This estimate tells sellers how much you are qualified to borrow and confirms that you are a ‘ready-to-close’ buyer.”

A straightforward financial history can lead to a home loan preapproval in 24-48 hours, essential for multi-bid offers. In 2024, affordability is top of mind for Utahns, with 50,000 monthly searches for mortgage qualification. Lenders compare your gross income to existing debt to determine your loan eligibility; use this for budgeting.

Mastering the Mortgage Pre-Approval Process

Education is a key component of this mid-journey phase, especially as interest rates fluctuate. Learning how to qualify for a mortgage loan involves more than just having a high salary. It requires a stable employment history and a healthy credit score to secure the best possible terms. When researching how to get approved for a mortgage loan, remember that your ‘mortgage-readiness’ depends heavily on your debt-to-income ratio. Lenders use this ratio to ensure you don’t become over-leveraged.

Education is a key component of this mid-journey phase, especially as interest rates fluctuate. Learning how to qualify for a mortgage loan involves more than just having a high salary. It requires a stable employment history and a healthy credit score to secure the best possible terms. When researching how to get approved for a mortgage loan, remember that your ‘mortgage-readiness’ depends heavily on your debt-to-income ratio. Lenders use this ratio to ensure you don’t become over-leveraged.

Many buyers also seek specific guidance on how to get approved for a home loan when they have unique circumstances, such as being self-employed or having a recent career change. No matter your situation, understanding the mortgage loan preapproval process is the best way to avoid surprises once you find a home you love. This process includes a deep dive into your assets and liabilities. I have found that being organized with your paperwork can shave days off the timeline. Utah’s 2024 market offers programs for first-time buyers with lower down payments or grants for easier ownership. First-time buyers often worry about approval due to shorter credit histories or smaller savings.

Lenders have evolved their models to help these buyers. The core question remains: ‘How do I get pre-approved for a home loan effectively?’ First-time buyers should start early and openly discuss any expected financial hurdles with their loan officer. By following the standard steps to get approved for a mortgage, they can leverage their mortgage preapproval to compete with more experienced investors. Understanding how to get approved for a mortgage loan is crucial for first-time buyers. It can make the difference between a rejected offer and a signed contract in a fast-paced neighborhood.

Steps to Get Approved for a Mortgage and Managing Approval Timelines

In the fast-moving 2024 market, mortgage approval time has become a critical metric for both buyers and sellers. Interest in this topic has spiked by 900%, as buyers need to know how quickly they can close to appeal to sellers. Sellers want a fast and certain transaction. The preapproval process can be quick but underwriting and appraisal take time. Plan for a 30-day closing. Being proactive with your documentation can reduce mortgage approval time and prevent last-minute delays.

Once you have your mortgage pre-approval estimate in hand, I recommend staying in constant contact with your lender. Address any additional requests for bank statements or income clarification immediately. This ensures you can move quickly and confidently when you find the right property in Utah’s competitive market. Navigating homeownership in 2024 requires a blend of digital convenience and procedural knowledge. That’s why I created this roadmap to guide you through every milestone.

From deciding how to get prequalified for a home loan to receiving your final keys, each step builds your future. Whether you choose an online home loan pre-approval for convenience or a face-to-face meeting with a local lender, getting approved for a mortgage is key to your financial security. Understanding how and where to get pre-approved positions you for success in any market. Don’t let the process intimidate you. Start today by seeking your mortgage prequalification estimate and take the first step toward your new Utah home.

If you’re shopping for a home in Utah, the best way to reduce stress (and write a stronger offer) is to get your financing ready before you fall in love with a listing. A real pre-approval helps you understand your budget, speeds up the offer process, and shows sellers you’re serious. This guide walks you through the process, the documents you’ll need, and how options like FHA, VA, and online applications fit in—so you can move quickly and confidently.

Mortgage Pre Approval Utah: What It Is and Why It Matters

Mortgage pre approval Utah means a lender has reviewed your financial information—typically income, assets, debts, and credit—and is willing to pre-approve you up to a certain loan amount (assuming nothing major changes before closing). This is different from a rough estimate because it’s based on documentation, not just a conversation. In many Utah markets, sellers and agents expect buyers to have a pre-approval letter ready, and it can make your offer feel safer and more credible.

If your main goal is to get pre approved Utah, start early. Even if you’re “just looking,” pre-approval gives you a realistic price range and helps you avoid wasting time on homes that don’t match your true buying power. It also gives you a chance to fix issues (like paperwork gaps or a debt-to-income problem) before you’re under pressure.

Home Loan Pre Approval vs. Pre-Qualification: Which One Do You Need?

Some buyers begin by trying to <strong>prequalify for home loan</strong> because it’s fast and low-commitment. Pre-qualification is usually an informal estimate based on what you report (income, debts, and general credit range). It can be helpful early on, and it’s why so many people search how to get prequalified for a home loan when they’re still exploring options.

But if you want to write offers, a home loan pre-approval is the stronger step because it involves verification. When you get pre-approved for a mortgage, the lender checks documents and runs credit, so the letter actually means something to sellers. If you’re serious about buying soon, you’ll typically want to move beyond pre-qualification and get pre-approved for a home loan before you start making big decisions.

Some buyers begin by trying to prequalify for home loan because it’s fast and low-commitment. Pre-qualification is usually an informal estimate based on what you report (income, debts, and general credit range). It can be helpful early on, and it’s why so many people search how to get prequalified for a home loan when they’re still exploring options.

But if you want to write offers, a home loan pre-approval is the stronger step because it involves verification. When you get pre-approved for a mortgage, the lender checks documents and runs credit, so the letter actually means something to sellers. If you’re serious about buying soon, you’ll typically want to move beyond pre-qualification and get pre-approved for a home loan before you start making big decisions.

How to Get Pre-Approved for a Home Loan in 5 Practical Steps

If you’ve been wondering how to get pre-approved for a home loan, this is the most straightforward path that works for most borrowers:

Pick a lender and complete the application

Upload your financial documents (income, assets, debts)

Authorize a credit check

Review loan options and confirm your comfortable payment range

Receive your letter and keep your finances stable while you shop

That process is also what people mean when they ask how to get preapproval for a home loan—the goal is a written letter you can use when making offers. You’ll often see similar phrases like mortgage loan pre approval and house loan pre approval; they’re different wording for the same milestone: you’ve been reviewed and are ready to buy within a certain range.

If you’re asking how I can get pre-approved for a home loan as quickly as possible, the #1 tip is to respond fast when the lender requests clarification (like a missing page of a bank statement, proof of employment, or explanation for a deposit). Delays usually happen when documents are incomplete or unclear.

What Is Needed to Get Pre Approved for a Mortgage: Your Document Checklist

People commonly ask what is needed to get pre-approved for a mortgage because they don’t want surprises. While lenders vary, you can usually prepare for these categories:

Identity verification (ID)

Proof of income (pay stubs, W-2s, or tax returns if self-employed)

Proof of assets (bank statements, retirement accounts, gift funds documentation if used)

Employment history details

A list of monthly debts (auto loans, student loans, credit cards)

Credit authorization (so the lender can review score and history)

This checklist is also what helps when you’re asking how to get pre-approved for a home mortgage—you’re proving you can repay the loan, and you have funds to complete the purchase.

If your question is more specific—like how to get pre-approved for a house or how to get pre-approved for a house loan—the same checklist applies. The “house” part just means you’re using the approval to shop for a property; the lender still evaluates the borrower the same way.

FHA and VA Options: FHA Loan Pre Approval and VA Home Loan Pre Approval

Your loan program can affect details (like down payment rules and documentation), but the structure of approval stays similar.

For FHA borrowers, FHA loan pre-approval is typically focused on verifying income, assets, and credit—then pairing you with FHA guidelines. You’ll also see the shorter phrase fha pre approval used interchangeably. FHA can be a fit for some buyers because it’s designed to widen access to homeownership, but it still requires careful documentation and underwriting.

For eligible military buyers, va home loan pre-approval can be a major advantage. You may also see va mortgage pre-approval used for the same concept. VA loans often require that you confirm your eligibility (commonly through a Certificate of Eligibility) and meet lender standards for credit, income, and occupancy.

Online Speed: Online Mortgage Pre Approval and How It Works

If convenience matters, <strong>online mortgage pre approval</strong> can reduce friction because you can upload documents through a secure portal, sign disclosures digitally, and track your progress without playing phone tag. Online doesn’t mean “less real”—your lender still verifies your financial profile. The benefit is speed and organization, especially if you’re juggling work, school, or moving timelines.

Many buyers start with an estimate and prequalify for a mortgage loan online first, then transition into full approval once they’re ready. If your goal is to move from “planning” to “offer-ready,” ask the lender what they need to convert a pre-qual into a full approval letter.

FAQ: The Most Common “How-To” Questions (Answered Clearly)

Q: How to get pre-approved for a mortgage loan? A: Apply, submit documents, authorize credit, and respond quickly to lender follow-ups. This is the cleanest path to a usable pre-approval letter.</p>

Q: Get pre-approved for a home mortgage (what should I do right now?) A: Gather your pay stubs/tax returns, bank statements, and debt info first—then apply. Being organized speeds everything up.</p>

Q: How to get preapproval for a mortgage if my credit needs work? A: A lender can often tell you what’s holding you back (high balances, recent late payments, or too much debt) and what to change before you reapply.

Q: Get pre approved for a mortgage and keep it valid A: Avoid opening new credit lines, making large unexplained deposits, or changing jobs during the process. Those things can trigger re-verification.

Entering the housing market as a new buyer is a significant milestone. Currently, in 2026, the landscape for home buyers in the Beehive State has shifted dramatically. If you are wondering, “how to qualify for a home loan first time buyer,” you aren’t alone. Fortunately, new state-level initiatives and shifting interest rates have changed the “old way” of buying a home. Therefore, saving 20% and walking into a bank is no longer the most efficient path. This roadmap helps you navigate the process like a pro. Ultimately, you can use these resources to get into your first home with less stress.

First time home buyer programs and State Assistance

A successful purchase begins with understanding local first time home buyer programs. In fact, Utah offers some of the most robust assistance in the country. The Utah Housing Corporation down payment assistance is a powerful tool in your arsenal. Specifically, this program helps buyers who have stable income and good credit. Consequently, it removes the need for a massive down payment for house costs.

Additionally, you should search for a specific First-time homebuyer grant Utah. Programs like the S.B. 240 initiative provide up to $20,000 for new construction. Indeed, this grant effectively wipes out the need for a massive upfront investment. Overall, these 1st time home buyer programs keep homeownership attainable for young families and professionals in our state.

Financial Readiness and the Qualifying Phase

Sit down with a professional before you start looking at listings. First, you must determine: how much mortgage can I qualify for? Many buyers browse homes based on a high-level estimate. However, they often find out later that their debt to income ratio for home loan requirements won’t support that price point. Because of this, understanding “how much would I qualify for a house” prevents heartbreak. Essentially, you should factor in current rates and your personal savings before you fall in love with a property.

To begin, use a house affordability calculator to play with different scenarios. However, remember that these tools often skip “hidden” costs. For example, a mortgage payment calculator with taxes gives a realistic view of your monthly budget. It includes property taxes and homeowners insurance. Once you are ready for a firm answer, the next step is to apply for a mortgage.

Navigating FHA Loans and Other Options

Many residents search for FHA loans first. Notably, these loans offer flexible credit requirements and a low 3.5% down payment. To qualify for FHA mortgage options, you must meet Utah FHA loan requirements. Typically, these include a 580+ credit score and a steady two-year work history.

Meanwhile, USDA loans offer an incredible zero-down path for those buying in rural areas. This includes parts of Tooele or Box Elder County. As a result, your success depends on partnering with the best mortgage lenders for first time buyers. These experts know how to “stack” loans with local grants.

The Approval Process: Prequalification vs Pre-approval

If you are just starting, you can seek a prequalify mortgage loan status. Basically, this gives you a ballpark estimate. However, a simple home loan pre-qualification isn’t enough in Utah’s competitive market. Instead, you need a formal mortgage pre approval. This verified document wins bidding wars. Importantly, it tells the seller that your financing is already vetted.

Learn how to get preapproval for a home loan to build confidence. Specifically, you should know how to get pre approved for a home mortgage before making an offer. Many buyers ask, “how can i get pre approved for a home loan?” or “how to get pre approved for a house loan?” In short, the answer is simple. Gather your tax returns, pay stubs, and bank statements. Then, let a lender run a full credit and asset review.

Final Steps: Applying for down payment assistance

Finally, once you are under contract, the final phase begins. Start applying for down payment assistance through the Utah Housing Corporation. Indeed, this step bridges the final gap. It ensures your first home owner loan or first time mortgage is fully funded. Soon, you will move from asking how to qualify for a home loan first time buyer to becoming a proud Utah homeowner.

Entering Utah’s housing market requires more than just finding the right property. it requires understanding how to finance it strategically. Whether you’re preparing to buy a home in Utah or planning long-term equity growth, knowing how FHA loans, refinancing options, and equity tools work together will put you in a stronger financial position.

This guide walks through the major financing options available to Utah buyers and explains how each decision impacts your long-term financial plan.

FHA Loans in Utah: Qualification, Credit Scores, and Loan Limits

For many buyers, FHA loans provide one of the most accessible paths to homeownership. These government-backed mortgages are especially helpful for borrowers with moderate income, limited savings, or credit challenges.

Those researching FHA loans for bad credit often find that FHA guidelines are more flexible than conventional programs. The typical FHA loan minimum credit score is lower than most traditional financing options, making it attractive for first-time buyers.

Understanding how to qualify for FHA loan programs requires reviewing income stability, debt-to-income ratio, and employment history. Before choosing FHA financing, buyers should evaluate the fha loan pros and cons, particularly mortgage insurance requirements. It’s also wise to compare FHA vs. conventional loan structures to determine which aligns best with your long-term financial goals. Additionally, county-specific FHA loan limits in Utah can influence how much you’re able to borrow, depending on where you plan to purchase.

Down Payment Assistance and First-Time Buyer Programs in Utah

One of the biggest obstacles for new homeowners is saving for a down payment. Fortunately, several first-time home buyer down payment assistance programs exist to reduce upfront costs.

Programs offering Utah first-time home buyer assistance and broader Utah down payment assistance programs help qualified buyers bridge the financial gap. Reviewing first-time home buyer requirementsearly ensures you’re fully prepared before entering the market.

If you’re still learning how to buy your first home, working with a local mortgage professional can clarify eligibility guidelines, documentation needs, and financing timelines.

In certain rural areas, a USDA loan Utah may also provide zero-down financing opportunities for eligible properties.

Monitoring Mortgage Rates and Evaluating Refinance Opportunities

Interest rates significantly affect monthly payments and long-term affordability. Keeping an eye on the mortgage rate forecast and reviewing a mortgage rate history chart can help you understand current market trends.

Choosing between a fixed vs adjustable mortgage is another critical decision. Fixed-rate loans offer payment stability, while adjustable-rate mortgages may offer lower introductory rates depending on market conditions.

After purchasing, many homeowners begin asking when they should refinance. To answer that, you must consider refinance closing costs, evaluate whether a no closing cost refinance makes sense, and compare current cash out refinance rates.

Some borrowers also compare refinancing vs. home equity loan options to determine which offers greater flexibility or lower overall borrowing costs.

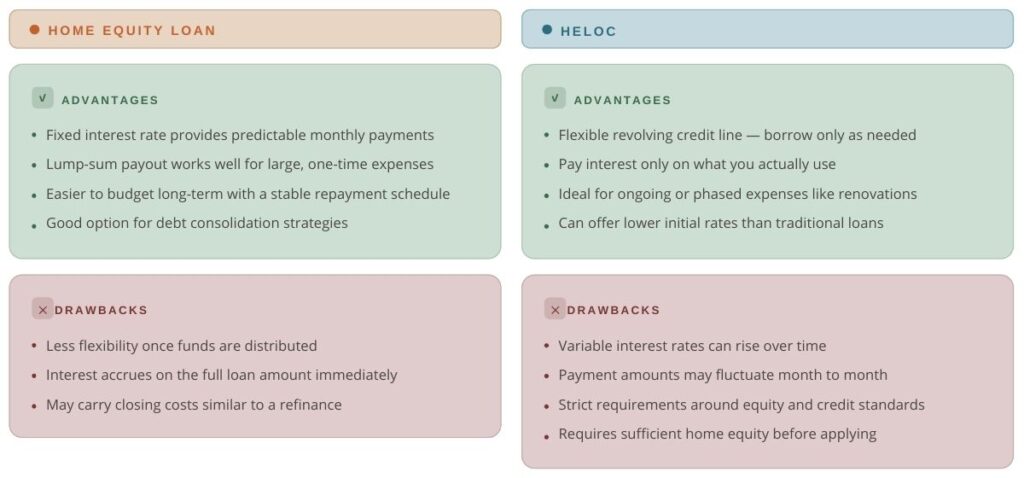

Home Equity Loan vs HELOC: Accessing Built-Up Equity

As property values increase, homeowners build equity that can later be accessed strategically. Before applying, it’s important to understand how much equity is needed to qualify for secondary financing.

When comparing home equity loans vs. HELOC products, the primary difference is structure. A traditional home equity loan provides a lump-sum payment with fixed repayment terms, while a revolving line of credit offers more flexibility. Evaluating HELOC vs. home equity loan options allows homeowners to match borrowing structure with financial goals.

Understanding typical HELOC requirements, including minimum credit thresholds, equity levels, and income documentation, improves your chances of approval.

Many borrowers choose a home equity loan for debt consolidation to reduce high-interest balances and simplify monthly payments.

Building a Sustainable Strategy

Successfully planning to buy a home in Utah involves more than securing loan approval. It requires understanding how FHA loans, Utah assistance programs, refinancing strategies, and equity tools fit into a long-term financial plan.

By monitoring rate trends, comparing loan structures (e.g., fixed vs. adjustable mortgages), evaluating refinance timing, and preparing for future equity access, you position yourself for financial stability and growth.

Working with experienced Utah mortgage professionals ensures you remain informed as market conditions evolve and your goals change.

If you’re thinking about buying a home in Utah, one of the smartest first steps you can take is using a mortgage calculator. A mortgage calculator Utah buyers rely on lets you plug in your loan amount, interest rate, and down payment to get a realistic picture of what your monthly payments might look like — before you ever set foot in a lender’s office. Understanding mortgage rates today makes those estimates even more accurate and helps you plan with confidence.

One of the most common questions among first-time buyers is, “How much home can I afford in Utah?” The answer depends on more than just your income. When you combine a mortgage calculator with a mortgage pre-approval, you get a much clearer financial picture. Lenders will look at your income, your debt-to-income ratio, and your credit history before issuing a pre-approval letter, and knowing those numbers ahead of time puts you in a stronger position from the start.

When running your numbers, make sure your calculations go beyond just the principal and interest. Mortgage closing costs in Utah, property taxes, homeowner’s insurance, and PMI — if your down payment is less than 20% — can all add meaningfully to your monthly expenses. For buyers exploring programs like FHA loans, Utah’s requirements may allow for a lower down payment, which will shift those estimates and open up options that might otherwise seem out of reach.

The type of loan you choose also plays a major role in what you’ll pay each month. A 30-year fixed mortgage gives you the stability of a consistent payment over the life of the loan. VA loan rates in Utah can offer significant savings for eligible veterans and service members. And for buyers looking outside of major metro areas, USDA loan eligibility in Utah can make rural homeownership much more accessible.

Using a mortgage calculator before you apply for a loan isn’t just a helpful exercise — it’s a way to avoid surprises during underwriting and walk into the process knowing exactly what you’re working with.

For borrowers with a 700 credit score, mortgage qualification becomes significantly more favorable compared to lower credit tiers. While a 700 score is generally considered “good,” approval still depends on more than just credit. Lenders evaluate income stability, debt obligations, employment history, and overall financial risk before determining how much mortgage you can qualify for.

Understanding how a mortgage with 700 credit score is evaluated helps borrowers prepare beyond simply checking their credit report.

What Does a 700 Credit Score Mean for Mortgage Approval?

A mortgage with 700 credit score typically qualifies borrowers for conventional loan programs with competitive interest rates. Compared to lower credit ranges, a 700 score often results in:

More favorable interest rates

Lower private mortgage insurance (PMI) costs

Stronger approval likelihood

Greater flexibility in down payment requirements

However, lenders still calculate your debt to income ratio for mortgage approval to ensure total monthly obligations remain within acceptable limits. A strong credit score improves eligibility, but excessive debt can reduce approval amounts.

This reinforces an important principle: credit score alone does not determine approval. Overall financial stability carries equal weight in the underwriting process.

Income and Debt Still Determine How Much You Can Qualify For

Even with solid credit, lenders analyze:

Gross monthly income

Total recurring debts

Employment consistency

Minimum income for mortgage approval standards

Your overall debt-to-income ratio

Borrowers often use tools like a mortgage calculator with down payment or a 30 year fixed mortgage calculator to estimate monthly obligations before formally applying. These tools provide a realistic payment expectation but do not replace full lender evaluation.

Ultimately, how much mortgage you can qualify for depends on the relationship between income, debt, and long-term repayment capacity.

Down Payment Strategy and Loan Structure

Down payment size also influences approval and loan terms. A larger down payment can:

Reduce monthly payment obligations

Lower PMI requirements

Strengthen underwriting confidence

Improve long-term affordability

First-time buyers may compare options using a mortgage calculator first time buyer bad credit tool to understand how interest rates shift across different credit brackets.

Even with a 700 score, optimizing down payment strategy can improve loan performance and financial flexibility.

What Else Affects Mortgage Affordability?

Beyond credit score, lenders consider:

Length of credit history

Recent credit activity

Existing loan balances

Stability of employment

Overall financial behavior

These factors collectively determine approval risk and influence final loan structure. Understanding what affects mortgage affordability allows borrowers with a 700 credit score to strengthen weak areas before applying.

Final Thoughts

A mortgage with 700 credit score provides access to strong lending opportunities, but it represents only one component of mortgage qualification. Income consistency, debt management, down payment size, and loan selection all influence final approval outcomes.

Borrowers who evaluate their full financial profile instead of relying solely on credit score position themselves for stronger long term affordability and sustainable homeownership.

Utah Mortgage Rates Today If you are searching for the best mortgage rates in Utah, it is important to understand how Utah mortgage rates today are determined. Rates change daily based on market conditions, credit score, loan type, and down payment amount. The 30 year fixed mortgage rates Utah option remains the most popular choice because it offers stable monthly payments and long-term predictability. When comparing offers, borrowers should also review mortgage closing costs Utah in addition to the interest rate. First Time Home Buyer Mortgage Utah Programs Utah offers several programs designed to help first-time buyers enter the market. A first time home buyer mortgage Utah program may include down payment assistance or flexible credit guidelines. Getting mortgage pre approval Utah early in the process helps buyers understand how much home can I afford Utah before making an offer. Sellers are also more likely to accept offers from pre-approved buyers. FHA, VA, and USDA Loan Options Government-backed loans provide flexible alternatives: FHA loan Utah requirements allow lower credit scores and smaller down payments. VA loan rates Utah offer competitive terms for eligible veterans and active military. USDA loan Utah eligibility supports buyers purchasing homes in qualified rural areas. Each option has unique qualification standards, so comparing lenders is important. HELOC Requirements and Home Equity Options Homeowners looking to access equity should understand HELOC requirements before applying. A home equity line of credit vs home equity loan comparison helps determine which option fits long-term financial goals. HELOC rates Utah and repayment structures vary by lender, so borrowers should review terms carefully.

Buying a home starts with one essential question: how much mortgage can I afford? While many buyers begin with a mortgage calculator with taxes and PMI or a mortgage calculator with down payment, lenders evaluate so much more than a simple monthly payment estimate. Income, debt obligations, credit score, and loan structure all determine your final approval amount.

Understanding the difference between how much mortgage can I get approved for and how much mortgage can I qualify for is critical. Approval depends on verified income, employment stability, credit history, and your debt-to-income ratio for mortgage approval.

Income-Based Mortgage Affordability

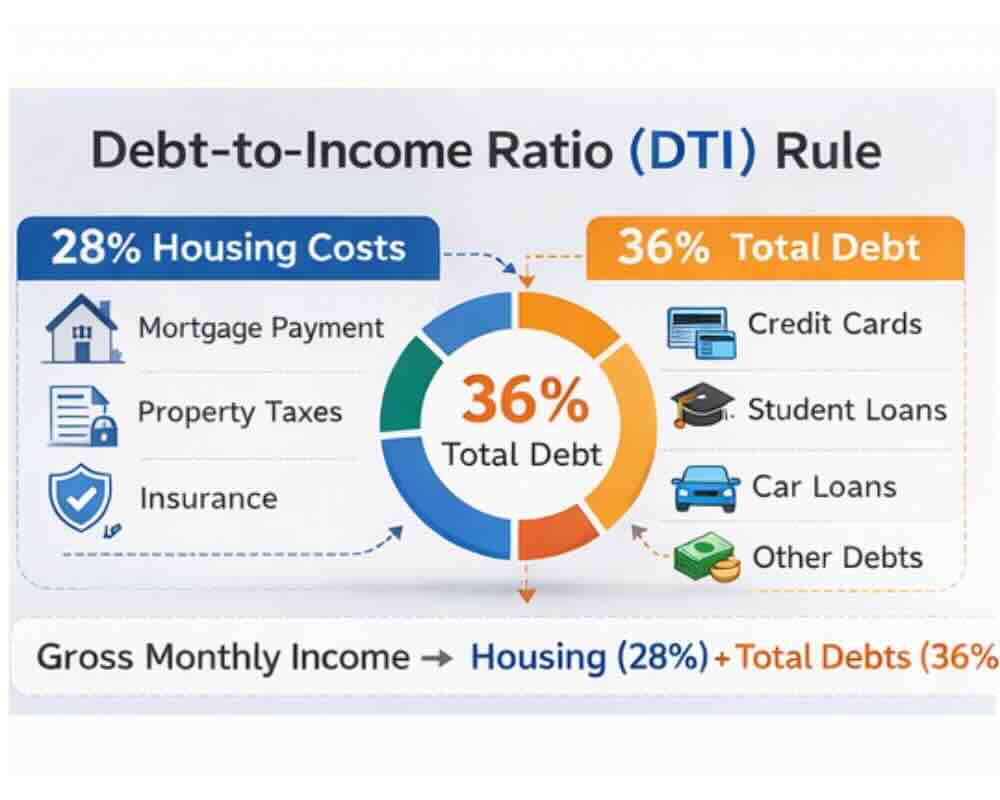

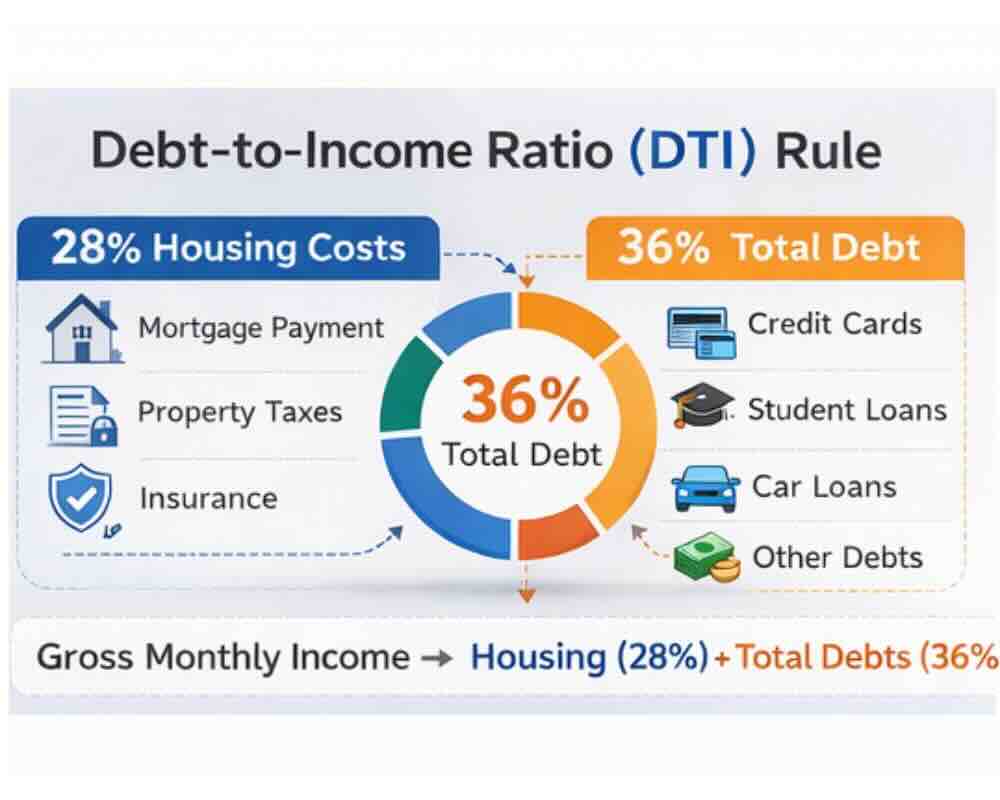

If you earn $65,000 annually, you may ask how much mortgage can I afford with 65k salary. Lenders often use the 28/36 rule, meaning no more than 28% of gross income should go toward housing and no more than 36% toward total debts.

For borrowers researching how much house can I afford 50k income, the same percentage guidelines apply, but the resulting maximum mortgage amount based on income will be lower.

Student loan debt also impacts affordability. Many buyers wonder how much house can I afford with student loans, since lenders calculate overall obligations using a mortgage affordability calculator debt to income ratio model. Some borrowers also prefer calculating conservatively and ask how much mortgage can I afford after taxes to ensure their budget remains comfortable.

Approval vs. Qualification Requirements

Lenders may require a certain minimum income for mortgage approval, but consistency of earnings often matters more than the raw number. If you are self-employed, a mortgage calculator for self-employed borrowers can help estimate potential affordability.

Those with commissions or fluctuating pay must understand how to calculate variable income for mortgage qualification. Most lenders review two years of income history to determine a stable average.

Credit Score and First-Time Buyer Considerations

Your credit profile significantly influences affordability. Securing a mortgage with 700 credit score generally provides access to competitive interest rates and better loan terms.

However, first-time buyers exploring a mortgage calculator first time buyer bad credit may see higher estimated payments due to increased risk. Lower-income households may also use a low-income mortgage calculator to determine realistic price ranges before beginning the application process.

Understanding the Full Monthly Payment

Many buyers only focus on principal and interest, but a realistic estimate requires more detail. Tools such as a mortgage calculator with insurance, mortgage calculator with HOA fees, and mortgage calculator including closing costs provide a clearer picture of total expenses.

A mortgage payment breakdown calculator separates principal, interest, taxes, insurance, and PMI. If purchasing with a partner, a dual income home loan calculator can demonstrate how combined earnings increase borrowing power.

Comparing options with a 30-year fixed mortgage calculator helps buyers understand long-term payment stability and total interest costs.

Ultimately, understanding what affects mortgage affordability ensures that you choose a loan that fits your financial goals rather than stretching to the maximum lender approval.