If you’re planning to buy a home in Utah, getting pre-approved for a mortgage in Utah is the key to securing your dream home. This guide covers FHA loan qualifications, ensuring you’re ready for Utah’s competitive market.

Why Mortgage Pre-Approval Matters in Utah?

Utah’s housing market (especially in Salt Lake City and Provo) is highly competitive. A pre-approval letter proves you’re a serious buyer and helps you:

Stand out in bidding wars

Lock in mortgage rates by credit score before they rise.

Calculate affordability with tools like a 300k mortgage payment calculator or mortgage affordability calculator income.

Step 1: Understand Pre-Qualification vs. Pre-Approval

Mortgage Pre-Qualification

Soft credit check (no impact on score).

Example: “estimate prequalification mortgage”.

Mortgage Pre-Approval

Hard credit pull + verified documents.

Example: “being pre approved for a home loan”.

💡 *Tip: Need a precise estimate? Use a 30-year fixed mortgage calculator or recast calculator mortgage.*

Step 2: Check Your Credit Score

Your mortgage rates in Utah depend heavily on your credit score:

<620 → Explore credit union refinance mortgage options.

740+ → Best rates (e.g., “top rated mortgage lenders 2021”).

620-699 → May need FHA loans (“what qualifies for fha home”).

Step 3: Compare Utah Mortgage Lenders

Lender Type

Best for

Keywords Examples

Banks

Traditional borrowers

“bank of america get pre approved”

Credit Union

Lower rates

“uw credit union pre approval”

Online Lenders

Speed

“preapproval rocket mortgage”

Local Lenders

Personalized service

“best mortgage company to use”

🔎 *Self-employed? See “best mortgage lenders for small business owners”.

Step 4: Submit Your Application

Documents Needed:

Pay stubs, tax returns, proof of income (“mortgage affordability calculator income”).

ID, bank statements, and asset proof.

Timing:

Apply 3-6 months early (“when should i apply for mortgage pre approval”).

Pre-approval lasts 60-90 days

Step 5: Explore Loan Types & Refinancing

FHA Loans

“Can I get a second FHA home loan?” → Yes, with restrictions.

Investment Properties

“Qualifying for investment property mortgage” requires higher down payments.

Refinancing

“Refinance mortgage lenders” can lower rates or tap equity.

Why Utah Mortgage Rates Today Matter More Than Ever.

In today’s competitive housing market, understanding Utah mortgage interest rates for first-time home buyers is essential for making informed decisions and securing favorable loan terms.. Whether you’re a seasoned homeowner or a first-time buyer, staying current with Utah mortgage interest rates today empowers you to lock in favorable financing terms.

Mortgage rates fluctuate based on a range of economic factors, including inflation trends, Federal Reserve policy, and lender risk assessments. While national averages provide a benchmark, Utah mortgage interest rates can vary significantly across lenders. Comparing current mortgage rates, 30-year fixed and mortgage rates today, FHA at the local level helps ensure that you secure a rate tailored to your needs.

Utah Mortgage Interest Rates Trends and 2025 Forecasts

As mortgage professionals, we are often asked: What are the projections for Utah home loan rates forecast for 2025? Based on market analysis, we anticipate relative rate stability in 2025, following the fluctuations seen throughout 2024. Prospective buyers and homeowners should closely monitor Utah mortgage interest rate trends this week via trusted sources like Freddie Mac’s PMMS and Utah-based lenders such as City Creek Mortgage. Utilizing tools like a Utah mortgage refinance calculator allows you to forecast payment scenarios and assess refinancing potential as market conditions evolve.

The Best Mortgage Lenders in Utah 2025: FHA, VA, and Jumbo Loans.

Navigating mortgage products can be complex, but understanding the nuances of each option is key. When researching the best mortgage lenders in Utah 2025, consider how your financial goals align with the following programs:

Utah FHA loan limits for 2025 have increased, allowing greater access for buyers using FHA-backed financing.

VA mortgage rates in Utah today remain a strong option for qualifying veterans, often featuring lower interest rates and no down payment.

Jumbo mortgage Utah requirements continue to evolve, with lenders requiring higher credit scores and thorough income documentation.

Those weighing FHA vs conventional mortgage Utah options should factor in long-term cost savings and qualification thresholds. For those with limited funds, programs offering Utah FHA down payment assistance provide critical support toward homeownership.

Getting Approved and Refinancing at Today’s Utah Mortgage Interest Rates

Knowing how to get approved for a mortgage in Utah includes maintaining a healthy credit profile, managing debt-to-income ratios, and collecting financial documentation early.

Homeowners evaluating mortgage rates refinance options should assess both cash out refinance Utah rates and traditional term refinancing. Not sure if it’s the right time? A Utah mortgage refinance calculator and platforms like FHA.com help clarify when to refinance mortgage Utah based on both market rates and your financial objectives.

Utah Mortgage Tools: Use These Calculators Before You Buy Before starting the home search, utilize tools that help shape your financial expectations.

A mortgage payment calculator Utah estimates your monthly obligation, while a home affordability calculator Utah factors in income, debt, and projected interest rates.

These resources are especially valuable if you’re exploring home equity loan interest rates or considering a move into Utah’s housing market for the first time.

FAQ – Utah Mortgage Interest Rates

Q: What are the current Utah mortgage rates for first-time buyers? A: Rates vary based on credit score, loan type, and market conditions. First-time buyers may qualify for competitive FHA and VA rates.

Q: Are Utah mortgage rates expected to drop in 2025? A: Based on current forecasts, experts anticipate a stable or slightly declining trend in interest rates through mid-2025.

This could be you! Read our Ultimate Guide to Tiny Home Mortgages to see how you can get your own Tiny House mortgage.

Everything You Need to Know About Tiny Home Loans in 2025

Are you ready to downsize, live more sustainably, or simplify your budget?

A tiny house mortgage can help. Lenders now offer several loan products for this growing market. Whether you plan to buy a finished home or order a custom build, you must understand each financing path.

Understanding Your Tiny House Financing Options

Tiny homes rarely fit the rules for a standard mortgage, so you need alternatives.

First, check banks, credit unions, and online lenders that market “tiny house loans.”

Next, compare personal loans; they fund quickly, yet their rates run higher.

Finally, look into tiny-house credit-union programs. These often feature lower fees and flexible terms.

One increasingly common route is to go through tiny house credit union mortgage programs, which may offer better terms, lower closing costs, and more flexibility than traditional banks. If your home is built on a permanent foundation, you may be able to apply for a fixed-rate mortgage, while those with mobile or on-wheels homes may need to consider a chattel loan for manufactured home.

Fixed-Rate vs. Chattel Loans

If your home sits on a permanent foundation, you can request a fixed-rate mortgage. Homes on wheels usually require a chattel loan, which treats the structure as personal property rather than real estate.

A chattel loan is a type of loan used to finance the purchase of movable personal property, often referred to as chattel, such as manufactured homes, vehicles, or equipment. It differs from a traditional mortgage, which is used for real estate, as chattel loans specifically target assets that are not permanently attached to land.

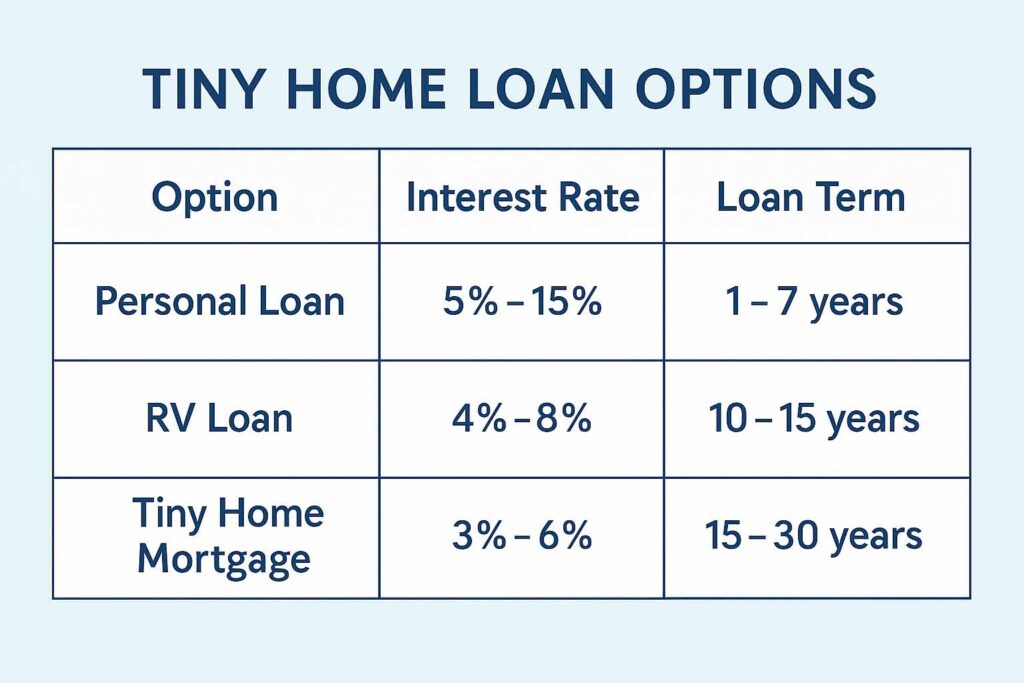

OPTION

INTEREST RATE

LOAN TERM

Personal Loan

5 – 15%

1 – 7 years

RV Loan

4 – 8%

10 – 15 years

Tiny Home Mortgage

3 – 6%

15 – 30 years

As you can see, there are a number of financing options depending on how long of long term you are interested in, each with different common interest rates. Check with a local credit union or bank for accurate mortgage rate information.

The smaller the house, the larger the life.” – Unknown

Are You Eligible for a FHA Manufactured Home Loan for your Tiny Home Mortgage?

Many first-time buyers are surprised to learn that government-backed programs such as the FHA manufactured home loan or VA manufactured home loan can apply to tiny or manufactured homes, especially if they meet certain size and foundation requirements. You’ll need to meet credit and loan requirements, and the home often must be permanently affixed to owned land.

If you qualify for a USDA manufactured home loan, you could benefit from zero down payment and low-interest terms, especially in rural areas. These programs are ideal for people who want to keep monthly payments manageable.

Planning Your Down Payment for a Tiny Home Mortgage

Most lenders want a 3 – 20% down payment. Your credit score drives that figure. Therefore, raise your score before you apply, and the lender may lower both the down payment and the mortgage-insurance premium. Use an online calculator to test payment scenarios, including taxes and escrow.

Use a mortgage calculator to estimate your monthly payments based on your interest rate, loan type, and loan estimate. Don’t forget to factor in property taxes, mortgage insurance, and escrow account costs. Check out our article on Mortgage Pre-Approval.

Modular Home vs. Tiny Home: A Quick Comparison

If you’re not 100% set on a tiny home, you might want to compare it to a modular home mortgage or manufactured home financing.

Modular homes are built in sections at a factory and later assembled on-site. They give you more space and, often, a smoother underwriting path. Rates can run a bit lower than tiny-home loans, yet zoning laws for modular builds stay strict. Consequently, verify local codes before you decide.

Interest rates and modular home loan rates are often slightly better than those for tiny homes. That said, modular home lenders still may require stricter building codes and zoning compliance.

The Role of Your Real Estate Agent and Lender

A knowledgeable real estate agent familiar with alternative housing is a must. They can help you find properties zoned for tiny homes and even connect you to manufactured home lenders or best manufactured home lenders who offer competitive rates.

Working with a mortgage broker or mortgage lender who understands tiny homes will make a big difference in navigating approval hurdles. Ask your broker to break down terms between an adjustable-rate mortgage and fixed-rate mortgage so you can decide what works best for your long-term goals.

Final Thoughts: Is a Tiny Home Right for You?

The home buying process for a tiny house may involve a few more hoops than a traditional purchase—but the rewards are worth it. Lower debt-to-income ratio requirements, smaller closing costs, and reduced monthly obligations make it an appealing choice for many modern buyers.

Whether you’re a minimalist, a first-time buyer, or simply ready for a change, a tiny house mortgage could be the start of your next great adventure.

This could be you! We hope you enjoyed learning about how you can get your own Tiny House mortgage.

External Links for More Information about Tiny Home Mortgages and Tiny House Mortgages

Cole Preece is an MBA and MSIS student at the University of Utah graduating in December 2025. Cole is a Utah local who enjoys exploring the mountains, forests, and beaches in the Rocky Mountains and Pacific Northwest.

Want to understand current mortgage rates in Utah today? This guide helps you compare, calculate, and lock in the best deal using real numbers and tools updated for 2025. Looking to buy or refinance in Utah? Explore the current mortgage rates today, compare top lenders, use our Utah mortgage calculator, and larn how to lock in the best rates for 2025. Many homebuyers are surprised by how much they can save by checking the current Utah home loan ratestoday rather than relying on national averages.

Current Mortgage interest rates in Utah Today: How to Compare, Calculate, and Lock in the Best Deal

Current rates for Utah mortgages Today: What to Expect

If you’re refinancing or buying your first home, understanding the Home financing options in Utah can help you lock in a better deal for your long-term goals. Mortgage pricing today can vary depending on your loan type, credit score, and lender. As of this week, 30-year fixed mortgage Utah rates average around 6.5%, while 15- year mortgage rates Utah sit closer to 5.9%. These rates can fluctuate daily, which is why many homebuyers are choosing to lock Home loan rates in Utah while they’re favorable. If you’re refinancing, refinance rates in Utah today follow a similar pattern, offering lower rates for shorter terms. Tools like a Utah refinance calc

Using a Utah Mortgage Calculator for Smarter Planning

Before applying, use a Utah mortgage calculator to estimate monthly payments. These tools allow you to plug in your loan amount, interest rate, and term length to forecast affordability. Many include options to estimate Utah home equity loan rates, taxes, and insurance—giving you a more realistic picture. Refinancing? Be sure to use a Utah cash-out refinance calculator if you’re looking toleverage your home equity for major purchases.

Compare Mortgage Rates From Utah Banks and Lenders

Choosing the best mortgage companies in Utah can make a huge difference in your loan experience. Some of the top-rated Utah mortgage lenders include City Creek Mortgage, Academy Mortgage, and Intercap Lending. Always compare mortgage rates from Utah banks, credit unions, and online brokers. Look for no closing cost mortgage Utah options, lowest down payment Utah mortgage offers, and pre-approval terms from Utah mortgage pre approval providers.

Exploring Loan Options – FHA, VA, Jumbo & More

Different loans mean different rates. Here’s a quick breakdown: Utah FHA loan rate today is often lower than conventional rates and great for first-time buyers with minimal down payments. VA loan rates Utah are exclusive to veterans and active-duty military, often with 0% down. Utah jumbo mortgage rates are needed for homes priced above county loan limits—expect slightly higher rates. Utah HELOC rates and Utah home equity loan rates let you tap into your home equity for renovations, debt payoff, or investments.

The Forecast – Utah Mortgage Rate Trends 2025

Wondering what’s next? According to experts, Utah mortgage rate predictions 2025 show potential stabilization, with Utah mortgage rate trends 2025 indicating a slow drop as inflation cools and demand evens out. Stay informed with a Utah mortgage rate chart from reliable financial sources to track monthly rate changes.

Final Tips – Locking the Best Mortgage Rate in Utah

Here’s how to snag the best current Loan interest rates in Utah: Apply for Utah mortgage pre approval to show you’re a serious buyer; monitor Utah mortgage rate forecast updates weekly; consider shorter loan terms for better rates (i.e., 15-year); ask about no closing cost mortgage Utah options to save upfront; and review and lock mortgage rate Utah when it dips.

Conclusion: Take Action With the Right Tools & Info

From using a Utah mortgage calculator to comparing Utah mortgage lenders, the tools are in your hands. Whether you’re buying your first home or refinancing with Utah cash out refinance rates, now is the time to make smart moves. Keep an eye on the Utah mortgage rate chart and remember to lock in rates when they align with your financial goals.

Frequently Asked Questions About Utah Mortgage interest rates

Should I lock in my mortgage rate now?

With rates still fluctuating, many Utah buyers are choosing to lock in their mortgage rate if they find one that fits their budget. Locking prevents you from being affected by rising rates between approval and closing.

What’s the difference between fixed and adjustable rates?

A fixed-rate mortgage means your interest rate stays the same throughout your loan term. An adjustable-rate mortgage (ARM) starts lower but may change after a few years based on market conditions.

Can I refinance if I just bought a home last year?

Yes! If rates have dropped or your credit has improved, refinancing—even within a year—can help you lower monthly payments or pull out equity through a cash-out refinance.

How to Use Our Utah Mortgage Calculator

Just plug in your loan amount, interest rate, and term length. You can also estimate property taxes, insurance, and even HOA fees for a more accurate view. Want to test a cash-out refi scenario? Adjust the loan amount to include equity withdrawal. The calculator updates instantly!

Still comparing options? Be sure to bookmark this page and check back weekly—we update our Utah mortgage rate trends every Friday to help you stay ahead in 2025.

Dreaming of owning your first home in the Beehive State? That’s an exciting milestone! First, understanding your first-time homebuyer mortgage in Utah is your most important step. Many potential homeowners start by looking at 30-year mortgage rates. Indeed, this is a common choice for home loans. However, you must learn much more to successfully navigate the Utah housing market. Specifically, consider unique local factors and available programs.

Therefore, this comprehensive guide will walk you through the essential aspects. We’ll cover everything from pre-approval to understanding different loan types. Moreover, we’ll help you navigate final costs. Ultimately, this ensures you’re well-equipped for your homeownership journey in Sandy, Utah, and beyond.

Kickstarting Your First-Time Homebuyer Journey with Utah Mortgage Pre-Approval

One of the very first things you’ll need to do is get pre-approved for a home loan in Utah. Do this even before you browse listings. Simply put, this isn’t just a suggestion; it’s a critical step that empowers you as a buyer. Pre-approval signals to sellers that you’re a serious, qualified candidate. As a result, this gives your offer significant weight in a competitive market.

To prepare, assemble a comprehensive Utah mortgage pre-approval checklist. Typically, this involves gathering recent pay stubs, bank statements, tax returns, and details on any existing debts. To get an early sense of your borrowing capacity, try using a mortgage pre-approval calculator online. Consequently, this can provide a preliminary estimate of what lenders might offer. It helps you set a realistic budget for your new home. For a quick estimate, try our Online Mortgage Calculator!

Exploring Diverse Utah Home Loans and Fulfilling Requirements

Utah offers a diverse landscape of home loans. In fact, each design meets varying financial circumstances and needs. For many embarking on a first-time buyer mortgage journey, government-backed programs often present the most advantageous paths.

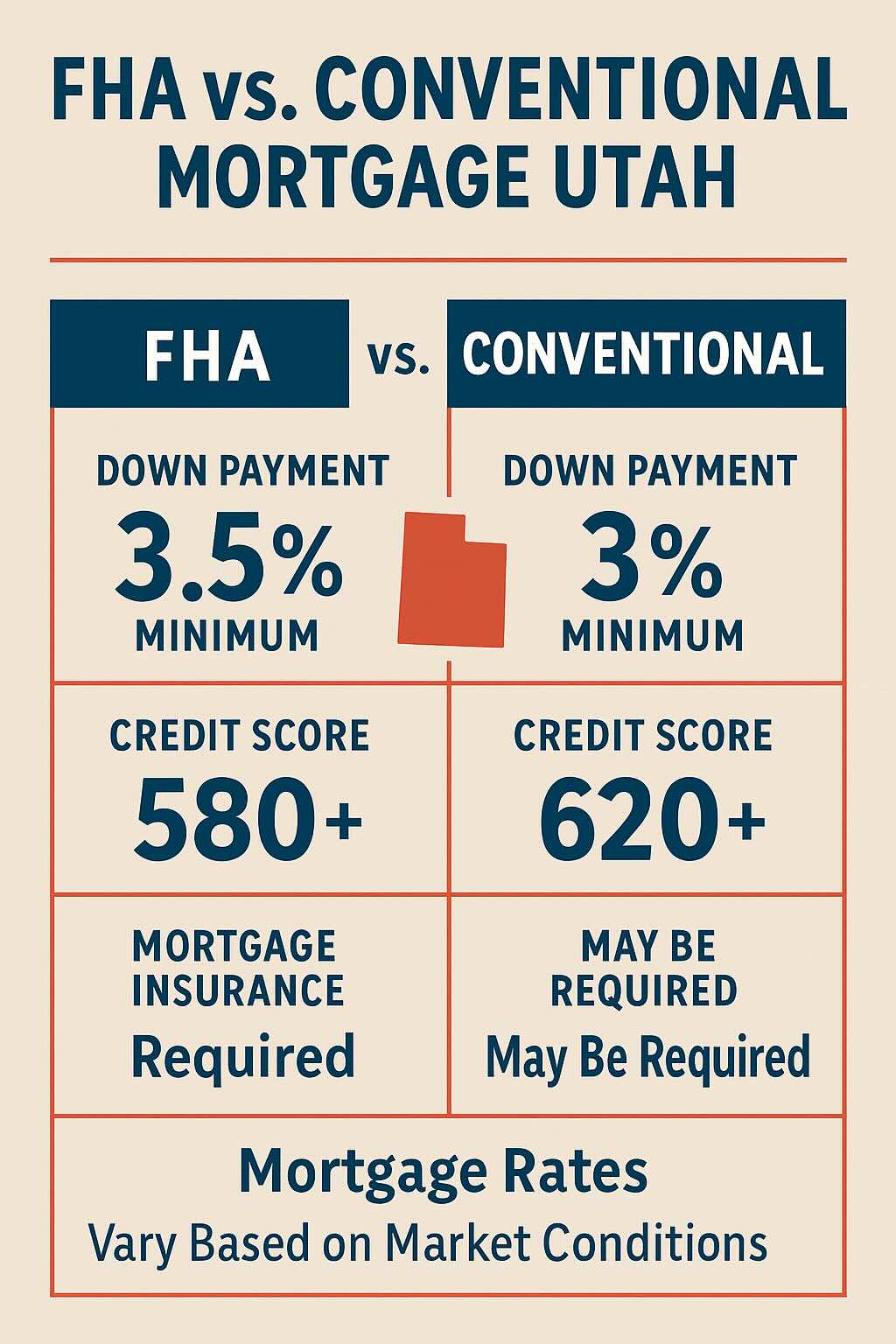

You must thoroughly understand FHA loan requirements in Utah 2024. These loans are popular for their lower down payment options and more flexible credit score guidelines. For example, Neighbors Bank typically requires a 3.5% down payment with a 580+ credit score for FHA loans (Neighbors Bank FHA Loan Guide).

Furthermore, if you’re a veteran or active service member, explore Utah VA home loan requirements. These can offer exceptional benefits, including no down payment and competitive interest rates (Veterans United VA Loan Eligibility). Similarly, for those looking in more rural areas, ask “do I qualify for a USDA loan in Utah?” This might lead to another excellent zero-down payment opportunity. Crucially, this program tailors for specific communities.

In summary, each of these programs comes with unique criteria. Therefore, consulting with a knowledgeable local mortgage professional is always recommended. They can help identify the best fit for your situation. Learn more about specific loan types on our Loan Programs Page.

Finding Competitive Rates and the Best Lenders in Utah

Securing your first-time homebuyer mortgage in Utah means more than just getting approved. Instead, it means finding the most favorable terms. To do this, diligently compare mortgage lenders in Utah. Everyone aims for the lowest mortgage rates in Utah today. Currently, 30-year fixed mortgages average around 6.93% as of June 21, 2025 (Bankrate Utah Mortgage Rates). However, you also must consider the lender’s overall service, fees, and reputation.

Don’t solely focus on advertised 30-year mortgage rates. Instead, look at the Annual Percentage Rate (APR). This provides a more complete picture of the loan’s true cost, including various fees. Seeking out Utah mortgage broker reviews can offer invaluable insights. Specifically, these reviews show other borrowers’ experiences. This helps you pinpoint the best mortgage lenders in Utah for first-time buyers who prioritize client satisfaction and transparency. A good mortgage broker can be a significant asset. After all, they often work with multiple lenders. This helps you secure the most competitive terms available.

Demystifying Mortgage Costs with Calculators and Financial Planning

As you move closer to making an offer, clearly understanding your home loan’s financial implications becomes paramount. While a simple mortgage calculator can quickly estimate your principal and interest payments, a more accurate picture requires a Utah mortgage calculator with taxes and insurance. This comprehensive tool factors in your estimated monthly property taxes and homeowner’s insurance premiums. Indeed, these are significant components of your total monthly housing expenses in Utah.

To help set a realistic budget for your home search, a mortgage affordability calculator will assess how much home you can truly afford. It bases this on your income, existing debts, and living expenses. Beyond monthly payments, remember to budget for average closing costs in Utah. These are the various fees associated with finalizing your mortgage and transferring property ownership. They typically range from 2.48% for sellers in Utah (Clever Real Estate Closing Costs) but generally 2-5% for buyers. For instance, these costs cover items like lender fees, title insurance, and appraisal costs. Being prepared for these upfront expenses is key to a smooth closing.

Navigating the Application Process and Future Refinancing Options

The culmination of your planning for a first-time homebuyer mortgage in Utah is the formal application process. Knowing exactly how to apply for a mortgage in Utah streamlines this final stage. This involves submitting all necessary documentation from your Utah mortgage pre-approval checklist. Then, you formally apply for the chosen loan program. Be prepared for a detailed review of your financial history and employment.

Understanding the Utah mortgage timeline from offer to close can help manage expectations. Generally, this period typically ranges from 30 to 60 days. It encompasses appraisals, inspections, and final underwriting.

For existing homeowners in Utah, or those who plan to be homeowners for many years, understanding how to refinance a mortgage in Utah is also valuable knowledge. A mortgage refinance calculator can illustrate potential savings or benefits. This comes from adjusting your current loan terms. Perhaps, you want to lower your interest rate, change your loan term, or access home equity. Options like refinancing a VA home loan in Utah offer specific advantages for eligible veterans. They can leverage their benefits again.

Navigating the mortgage landscape can be overwhelming, especially with so many loan types, lenders, and rate options. Whether you’re a first-time homebuyer, a low-income applicant, or someone searching for the best mortgage loans in Utah, understanding your options is key to securing your dream home. This guide walks you through loan types, where to find them, and how to choose the right fit for your financial situation.

Understanding the Types of Mortgage Loans

Before diving into specific programs, it’s essential to understand the various mortgage loan types. The most common include:

These types of mortgage loans serve a variety of borrowers, from those with excellent credit to those with non-traditional income sources.

Low Interest Mortgage Loans: A Smart Financial Move

Low interest mortgage loans can save you thousands over time. They’re especially beneficial when rates are low. If you’re asking, “When will mortgage rates go down?” monitor the market closely and lock in rates during dips. Credit union mortgage loans often come with lower interest than traditional bank loans, making them a smart alternative.

Best Mortgage Loans for First-Time Buyers

First time mortgage loans help ease the financial pressure for new homeowners. Many Utah programs offer 0 down and low income mortgage loansto support first-time buyers. These easy mortgage loans are often backed by state or federal programs, reducing risk for lenders and improving access for borrowers.

No Income and Bank Statement Mortgage Loans

For self-employed individuals or those with variable income, traditional mortgage applications can be difficult. This is where bank statement mortgage loans and no income mortgage loans come into play. These options allow you to qualify based on your financial history rather than your W-2 or tax returns.

Guaranteed and Reverse Mortgage Loans

Guaranteed mortgage loans, such as those backed by FHA or VA programs, offer added security. For older homeowners, the best reverse mortgage loans let you access home equity without moving. This option can support retirees who need extra income.

Different Mortgage Loans for Unique Needs

Every borrower is different, which is why different types of mortgage loans exist. From cheap mortgage loans to applying for multiple mortgage loans at once, having choices ensures you find a loan tailored to your situation. For example, some may benefit more from low interest rate mortgage loans, while others seek easy to get mortgage loans with minimal paperwork.

Finding the Best Mortgage Loans Near Me

When searching for the best mortgage loans near me, consider working with top lenders for mortgage loans in Utah. These include national banks, local credit unions, and specialized mortgage companies. Some of the best companies for home mortgage loans have robust online platforms, transparent terms, and personalized service.

Best Way to Apply for Mortgage Loans

The best way to apply for mortgage loans is by preparing your financial documents in advance, comparing loan products, and getting pre-approved. Many online platforms make it easy to apply, while local mortgage brokers can offer tailored advice. Applying for multiple mortgage loans can also help you compare offers and choose the most favorable terms.

Compare Top Utah Lenders

Top Utah mortgage lenders offer competitive rates and strong customer service. Look for lenders with great reviews, responsive loan officers, and a variety of options like low income, first-time buyer, and 0 down mortgage loans. You can explore options via Utah Housing Corporation and local credit unions like Mountain America Credit Union.

Mortgage for Bad Credit: Is It Possible?

Yes, you can still qualify for a mortgage for bad credit. Many lenders offer programs specifically designed for those with credit challenges, including FHA and subprime loans. These easy to get mortgage loans typically come with higher interest rates, but they provide a pathway to homeownership while rebuilding your credit.

Monitoring Rates: When Will Mortgage Rates Go Down?

One of the most frequently asked questions is, “when will mortgage rates go down?” While no one can predict the market perfectly, keeping an eye on economic indicators, inflation data, and Federal Reserve decisions can help you time your application for the most favorable outcome.

Conclusion: Your Roadmap to the Best Mortgage Loans

From low interest mortgage loans to bank statement mortgage loans and everything in between, the Utah mortgage market offers a wealth of options. By understanding the different mortgage loans available and aligning them with your financial needs, you can secure the best mortgage loans for your situation. Whether you’re searching for mortgage loans near me, applying for multiple mortgage loans, or seeking mortgage for bad credit, being informed is your best asset.

Explore your options, connect with top lenders for mortgage loans, and take the next step toward homeownership today.

Explore current mortgage rates in Utah with expert tips, home loan comparisons, lender insights, and market trends. Learn how to secure the best rate in 2025.

Starting the home buying process in Utah? Understanding mortgage rates in Utah is one of the most important steps in making a smart financial decision. In this post, we’ll explain how Utah home loan rates work, explore factors affecting rate fluctuations, and provide practical tips on getting the best rate—whether you’re a first-time buyer or refinancing your home.

Current Mortgage Rates in Utah

If you’re looking to purchase a home in Salt Lake City, Provo, or anywhere in between, knowing the current mortgage rates in Utah can help you time your decision. As of mid-2025, Utah mortgage interest rates hover between 6.25%–6.75% for 30-year fixed loans, depending on your credit score and down payment.

Factors influencing today’s rates include:

Federal Reserve interest rate trends

Utah’s economic growth and housing demand

Your personal creditworthiness

Tip: Use a mortgage rate calculator Utah to get an estimate before applying.

Best Mortgage Lenders in Utah

Securing a low mortgage rate also means choosing the best mortgage lenders in Utah. Local banks, credit unions, and online lenders all compete for borrowers, offering different terms and perks.

Some top-reviewed lenders in 2025 include:

Mountain America Credit Union

Zions Bank

Rocket Mortgage

Guild Mortgage (popular for FHA loans in Utah)

For competitive options, also check out home loan programs in Utah supported by state and federal grants. First-time buyers may benefit from Utah Housing Corp programs or VA home loans Utah for veterans.

How to get a Low Mortgage Rate in Utah

To secure a competitive mortgage refinance rate in Utah or new home loan, focus on improving the following:

Your credit score (above 700 is ideal)

Your debt-to-income ratio

The size of your down payment

Type of loan (fixed vs. adjustable)

Working with a mortgage broker Utah locals trust can help you compare options. Also, watch for Utah mortgage rate trends, especially around major Fed announcements.

Pro tip: Lock your rate if the market looks volatile.

Utah Mortgage Rate Forecast and Trends

In 2025, Utah home mortgage rates are expected to fluctuate moderately due to inflation control efforts and economic shifts. While the rates are still higher than pre-pandemic levels, many analysts predict some softening later in the year.

Follow resources like Bankrate Utah or Freddie Mac to stay informed. Also consider talking to a local agent who can help you navigate mortgage loan options in Utah that fit your situation.

Mortgage Resources for Utah Homebuyers

Whether you’re looking for conventional loans Utah, Utah FHA loan requirements, or exploring Utah mortgage lenders for first-time buyers, be sure to check these tools:

Before shopping for homes or applying for a loan, securing a mortgage preapproval is a critical first step. A preapproval gives you a clear sense of your purchasing power and strengthens your offer in a competitive housing market. Most mortgage lenders in Utah require preapproval before they’ll lock in current mortgage rates. During this process, a lender will evaluate your income, credit score, outstanding debt, and assets. Unlike a prequalification, preapproval is more comprehensive and carries more weight with sellers and agents.

Comparing the Best Mortgage Lenders in Utah

Finding the best mortgage lenders requires more than rate shopping. You should also evaluate loan options, fees, support quality, and approval times. Gathering multiple mortgage quotes from both online and local institutions can help you identify the most favorable terms. Working with a mortgage broker near me can streamline this process even further. Brokers often provide access to exclusive loan products, including government-backed options such as:

FHA loans – ideal for first-time buyers

VA home loans – for veterans and service members

USDA loans – for buyers in rural areas

Each loan program offers different benefits, including lower interest rates or reduced down payment requirements, making them worth exploring based on your eligibility.

Understanding Your Mortgage and Equity Options

Most Utah buyers opt for fixed-rate mortgages, which lock in the mortgage interest rate for the life of the loan. Adjustable-rate mortgages may offer initially lower payments but come with the risk of future rate increases. When evaluating the best mortgage rates, it’s also important to compare the home loan interest rates available from different lenders.

For current homeowners, refinancing can be a valuable option. A refinance home loan can reduce your monthly payments or allow you to pay off your loan sooner. A cash out refinance lets you access your home’s equity for large expenses. If you want to keep your existing mortgage, you might consider a home equity loan or a HELOC. Although heloc rates can vary, these lines of credit offer flexibility for renovations or recurring costs.

Some of the best heloc lenders offer competitive terms for borrowers with strong credit profiles. Comparing their offers alongside second mortgage options will help you make a well-informed decision.

Today’s Mortgage Rates in Utah

Given the pace of market changes, it’s important to regularly monitor mortgage rates today. Even small shifts in interest rates can impact your monthly payments. Utah-based lenders may also offer competitive refinance rates, particularly if your credit has improved or your home has appreciated in value.

Using tools like Bankrate or local lender calculators, you can compare offers based on real-time data and better understand how your loan choice aligns with your financial plans.

Tips for Utah Home Buyers

If you’re among the many home buyers entering the Utah market for the first time, don’t overlook the state and federal programs designed to support new buyers. Benefits include:

Lower interest rates for first-time homebuyers

Down payment and closing cost assistance

Loan programs with more flexible credit requirements

Whether you’re applying for a mortgage loan or exploring home improvement loans, it’s important to apply for a mortgage early so you can address any potential financing issues before making an offer.

Final Thoughts: Make Your Mortgage Strategy Work for You

Securing the right mortgage doesn’t have to be overwhelming. Whether you’re looking into mortgage refinancing, exploring second mortgage options, or searching for the best home equity loans, knowledge is power.

Start by getting preapproved. Then, take the time to compare VA loan rates, home loan interest rates, and the latest offers from the best mortgage lenders. With this approach, you’ll be in a position to make confident, well-informed financial decisions about your home

Whether you’re preparing to apply for a mortgage, considering mortgage refinancing, or buying your first home, understanding mortgage rates today in Utah is crucial. Interest rates can fluctuate daily due to economic changes, and staying informed about current mortgage rates specific to Utah can help you make smarter financial choices. This guide breaks down everything you need to know about tracking Utah’s mortgage rate updates, exploring loan options, and using helpful tools to plan your path to homeownership.

Understanding Current Mortgage Rates in Utah

When it comes to mortgages, the numbers matter. Keeping track of mortgage rates today 30-year fixed loans is especially important, as these rates are the most common benchmark for borrowers in Utah. While national trends affect these rates, local economic factors and lender competition also play a big role.

If you’re thinking about mortgage refinancing, make sure to monitor mortgage rates today refinance to see if you can secure better terms. Comparing refinance mortgage rates from various mortgage lenders near me will give you an edge in finding the best mortgage rates that fit your financial goals.

For broader context, you can visit Bankrate’s Mortgage Rates Page to see nationwide trends. But don’t forget to check local lenders for the most relevant offers in Utah.

How to Apply for a Mortgage in Utah: A Beginner’s Guide

(Insert picture 2: mortgage rate.jpg) (Description: Utah style family neighborhood house with mountains behind it)

If you’re a first-time buyer, the process of applying for a home loan can feel overwhelming. The good news is that Utah offers multiple first-time home buyer programs designed to ease the financial burden and guide you through the process.

Your journey usually starts with mortgage prequalification, which helps determine how much mortgage can I afford. Using a mortgage payment calculator during this phase can give you a realistic idea of your future monthly payments based on current mortgage interest rates and loan terms.

Veterans have additional options with VA mortgage rates, which often come with lower interest rates and no down payment requirements. Wondering what the best mortgage option is for me? It depends on your financial situation and goals, but exploring all programs available in Utah will help you find the perfect fit.

For more details on these programs, check out the Utah Housing Corporation’s First Time Home Buyer Program.

Comparing Mortgage Rate Options in Utah

(Insert picture 3: Second mortgage.jpg) (Description: Sign pointing toward neighborhood with Utah foothills behind it)

Making the right choice requires a thorough mortgage rate comparison. Utah homebuyers typically consider conventional loans, FHA, USDA, and VA loans, each with its own benefits and eligibility criteria.

If you already own a home, you might also explore second mortgage rates to tap into your home equity. For veterans, reviewing current VA mortgage rates can unlock some of the most favorable financing available.

Don’t just focus on interest rates — fees, loan terms, and lender reputation are equally important. Remember, the question of what is the best mortgage option for me can only be answered after evaluating all these factors.

Why Staying Updated on Utah Mortgage Rates Matters

The mortgage market is dynamic, and mortgage interest rates today can change quickly based on economic shifts. Staying informed about the latest 30-year mortgage rates and refinancing opportunities can save you thousands over the life of your loan.

Tools like the mortgage payment calculator found on MortgageRateUtah.com make it easy to estimate your payments and compare different scenarios. Also, connecting with local mortgage lenders near me ensures you get personalized advice tailored to Utah’s market.

Use Tools to Your Advantage

Tools like the mortgage payment calculator found on MortgageRateUtah.com make it easy to estimate your payments and compare different scenarios.

Work with Local Experts

Also, connecting with local mortgage lenders near me ensures you get personalized advice tailored to Utah’s market.

Buying your first home is an exciting milestone, but it can also be overwhelming. As a first time home buyer, you may have many questions about mortgage rates, loans, and the steps involved in the home buying process. This guide will help you navigate the journey of becoming a homeowner in Utah.

Understanding Mortgage Rates in Utah for First Time Home Buyers

Mortgage rates play a crucial role in determining your monthly payments and the overall cost of your home. As a first time home buyer, it’s essential to understand how mortgage rates work and how to find the best rates in Utah. Comparing mortgage rates from different lenders can help you save money in the long run.

Loan Options for First Time Home Buyers

There are several loan options available for first time home buyers in Utah. These include FHA loans, USDA loans, VA loans, and conventional loans. Each loan type has its own eligibility requirements, benefits, and drawbacks. It’s important to research and choose the loan that best fits your financial situation and home buying goals.

Down Payment Assistance for First Time Home Buyers

One of the biggest challenges for first time home buyers is saving for a down payment. Fortunately, there are down payment assistance programs available in Utah that can help you cover this cost. These programs offer grants, loans, and other financial assistance to eligible buyers.

Affordable Housing Loans for First Time Home Buyers

Affordable housing loans are designed to help low- and moderate-income families achieve homeownership. As a first time home buyer, you may qualify for these loans, which often come with lower interest rates and more flexible terms. Researching affordable housing loan options can help you find a home that fits your budget.

Minimum Down Payment Requirements for First Time Home Buyers

The minimum down payment required for a home purchase varies depending on the loan type and lender. For first time home buyers, some loans offer low down payment options, such as 3% or even 0% down. Understanding the minimum down payment requirements can help you plan your finances and determine how much you need to save.

How Much Mortgage Can a First Time Home Buyer Afford?

Determining how much mortgage you can afford is a crucial step in the home buying process. As a first time home buyer, you’ll need to consider your income, expenses, and other financial obligations. Using a mortgage calculator can help you estimate your monthly payments and find a home within your budget.

Getting Preapproved for a Mortgage as a First Time Home Buyer

Getting preapproved for a mortgage is an important step for first time home buyers. Preapproval shows sellers that you are a serious buyer and gives you a clear idea of how much you can borrow. The preapproval process involves submitting financial documents and undergoing a credit check.

Mortgage Eligibility for First Time Home Buyers

To qualify for a mortgage, first time home buyers need to meet certain eligibility criteria. Lenders will consider factors such as your credit score, income, employment history, and debt-to-income ratio. Improving your credit score and reducing your debt can increase your chances of getting approved for a mortgage.

Credit Score Requirements for First Time Home Buyers

Your credit score is a key factor in determining your mortgage eligibility and interest rate. First time home buyers with higher credit scores are more likely to qualify for better loan terms. It’s important to check your credit report, address any errors, and take steps to improve your credit score before applying for a mortgage.

How Long Does Mortgage Approval Take for First Time Home Buyers?

The mortgage approval process can take anywhere from a few weeks to a few months. As a first time home buyer, it’s important to be prepared for this timeline and stay in communication with your lender. Providing all required documents promptly and responding to any requests can help expedite the process.

Understanding Closing Costs for First Time Home Buyers

Closing costs are the fees and expenses associated with finalizing your home purchase. These costs can include appraisal fees, title insurance, and attorney fees. First time home buyers should budget for closing costs, which typically range from 2% to 5% of the home’s purchase price.

Loan Estimate for First Time Home Buyers

A loan estimate is a document that provides an overview of the loan terms, interest rate, monthly payments, and closing costs. First time home buyers will receive a loan estimate after applying for a mortgage. Reviewing the loan estimate carefully can help you understand the total cost of your loan and make informed decisions.

Mortgage Insurance for First Time Home Buyers

Mortgage insurance is required for certain types of loans, especially those with low down payments. First time home buyers should be aware of the cost of mortgage insurance and how it affects their monthly payments. Some loans allow you to cancel mortgage insurance once you reach a certain level of equity in your home.

Escrow in Mortgage for First Time Home Buyers

Escrow is an account used to hold funds for property taxes and homeowners insurance. As a first time home buyer, you’ll make monthly escrow payments along with your mortgage payment. Understanding how escrow works can help you manage your finances and ensure that your property taxes and insurance are paid on time.

Loan Amortization Schedule for First Time Home Buyers

A loan amortization schedule shows the breakdown of each mortgage payment, including the principal and interest. First time home buyers can use this schedule to see how their loan balance decreases over time. Understanding loan amortization can help you plan for the future and make extra payments to pay off your mortgage faster.

Mortgage Glossary for First Time Home Buyers

The mortgage process involves many terms and concepts that may be unfamiliar to first time home buyers. A mortgage glossary can help you understand key terms such as APR, PMI, and DTI. Familiarizing yourself with these terms can make the home buying process less confusing and more manageable.

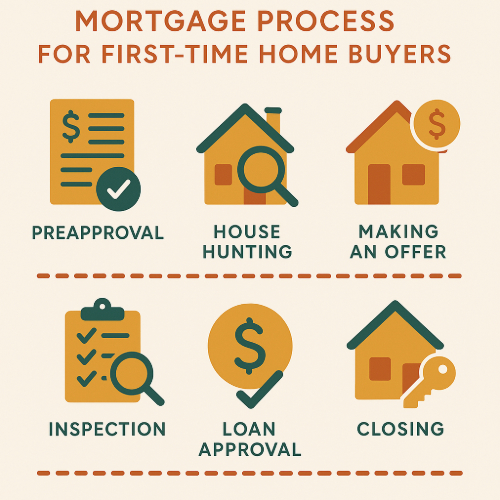

The Mortgage Process Step by Step for First Time Home Buyers

The mortgage process can be complex, but breaking it down into steps can make it more manageable for first time home buyers. This section will guide you through the process, from getting preapproved to closing on your home. Understanding each step can help you stay organized and confident throughout your home buying journey.

Working with a Mortgage Broker in Salt Lake City for First Time Home Buyers

A mortgage broker can help first time home buyers find the best loan options and navigate the mortgage process. Working with a local mortgage broker in Salt Lake City can provide personalized assistance and access to a wide range of lenders.

By following this guide, first time home buyers in Utah can navigate the home buying process with confidence and make informed decisions. Whether you’re looking for the best mortgage rates, down payment assistance, or loan options, this guide has you covered. Happy home buying!